What are you looking for?

Get help straight from our team...

Connecticut Loan Broker and Real Estate Agency Dual Authority

Compliance

Connecticut Loan Broker and Real Estate Agency Dual Authority

Although dual authority is allowed, compensation is limited when collecting fees for both services.

Last updated on 03 Nov, 2025

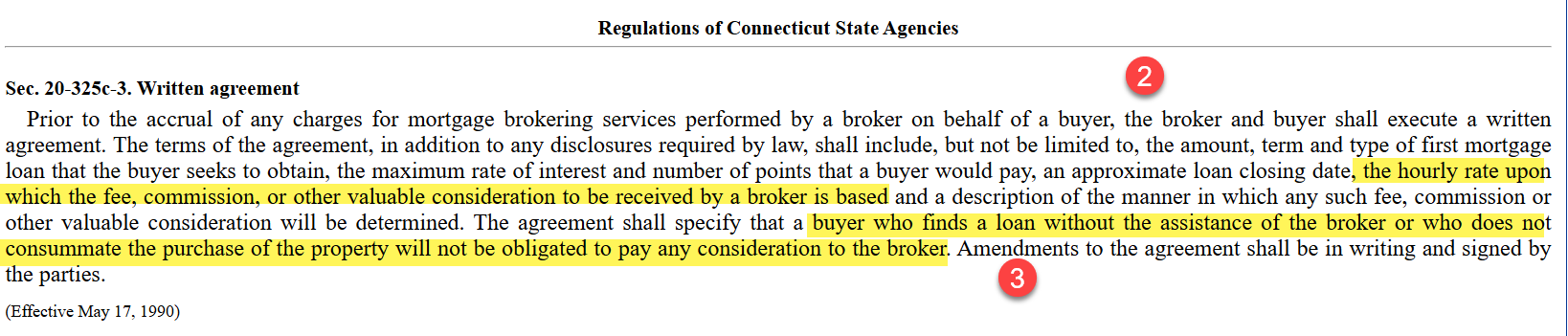

Connecticut Requirement - Flat fee mortgage broker compensation only, with an hourly rate calculation and a disclaimer that the borrower can obtain their own mortgage, and that fee is not due if the broker's loan does not close. In addition, you must demonstrate that you are shopping for the best option.

1) What CT law requires (quick snapshot)

If you act as the buyer’s real estate licensee and you assist in negotiating/soliciting/arranging/placing/finding the first mortgage loan on the same sale, your compensation for that mortgage-assistance work must be based on a reasonable hourly rate, not points or other market-based fees.

Legal Information Institute

You and the buyer must sign a written agreement before any charges accrue; it must state the hourly rate and how the fee will be determined. It must also tell the buyer they owe nothing if they find a loan on their own or the purchase doesn’t close.

You must keep time records and give the buyer an itemized invoice showing the hourly rate and hours spent on each service before receiving any compensation. Keep the invoice and time record for two years.

Legal Information Institute

By statute, any such fee must relate to services actually performed, may not be a referral fee, and must be paid directly by the buyer (not from loan proceeds at closing).

Justia Law

2) Compute a defensible “average hourly rate” for Connecticut

Because “mortgage broker” is often commission-based, we anchor the rate to the best objective wage data and then “load” it to a reasonable, billable hourly rate.

Step A — Market wage in CT (Loan Officers, SOC 13-2072):

BLS May 2023 mean hourly wage in Connecticut = $45.84. (BLS’s “Loan Officers” category includes mortgage loan officers/brokers.)

Bureau of Labor Statistics

Step B — Load for typical benefits (objective national ratio):

BLS Employer Costs for Employee Compensation (Mar 2025) shows wages are 70.3% of total compensation and benefits 29.7% in private industry. That implies a loaded comp = wage ÷ 0.703.

Loaded comp ≈ $45.84 ÷ 0.703 = $65.21 per hour.

Bureau of Labor Statistics

Step C — Minimal overhead + modest margin (professional services):

Add 15% overhead (licensing, E&O, software, admin) and 10% operating margin:

Billable rate ≈ $65.21 × 1.15 × 1.10 = $82.49/hour → recommend posting $82.50/hour.

Result: A documented, reasonable CT mortgage-assistance hourly rate = $82.50 (based on BLS CT wages, BLS benefits ratios, plus modest overhead/margin).

(For context only, private job boards sometimes show ~$40–$43/hr statewide; methodology varies and is less defensible than BLS. Your BLS-anchored calculation is stronger for compliance files.)

ZipRecruiter

3) Time itemization by mortgage-process step (use for estimates & invoicing)

These are conservative estimated hours for a typical purchase loan. The final invoice must reflect actual time entries per task.

Phase Billable activities (examples CT recognizes) Est. hours (range)

Conflict check & disclosure setup Confirm dual-role disclosures; open matter; compliance check 0.25–0.50

Initial consult & needs analysis Discuss financing options; scenario planning 0.50–1.00

Pre-qual analysis Income/asset review, DTI, pricing comparisons 1.00–2.00

Lender shopping Contact/compare lenders, program fit 0.50–1.00

Application intake Complete 1003, e-consents, explain disclosures 1.00–1.50

Docs checklist & collection Request/review paystubs, W-2s, VOE/VOI, assets 1.00–2.50

AUS & packaging AUS run(s), structure file, notes to UW 0.50–1.00

Submission to lender Upload, tie-outs, submit 0.50–1.00

Rate lock coordination Lock counseling and execution (if applicable) 0.25–0.50

3rd-party orders Appraisal scheduling, VOE/VOA follow-ups 0.50–1.00

Conditions clearing UW conditions, resubmits, pipeline updates 2.00–3.00

Closing coordination CD review, balances to close, scheduling 0.50–1.00

Post-closing QC File wrap, retention, QC log 0.25–0.50

Estimated total range: 8.25–15.50 hours.

At $82.50/hour, that’s about $681–$1,279 for a typical file (actuals may be lower/higher depending on complexity).

Note: CT expressly treats time spent “discussing financing options, completing applications, negotiating with prospective lenders, and performing underwriting activities” as bona fide hourly work. Keep contemporaneous time logs with short task notes.